I get this question a lot, from founders, families, and their advisors alike:

“What is the net worth trigger for a family office?”

$50 million?

$500 million?

$1 billion?

If you ask ten people in the world of private wealth, you will get ten different answers, each shaped by their own experience, their client base, and the lens of expertise through which they see the problem.

But these are the wrong questions.

The idea that a family office is activated by hitting a specific number is one of the most persistent and expensive misconceptions in private wealth.

And it stems from a fundamental misunderstanding of what a family office actually is.

The investment manager will tell you a family office is about portfolio governance and manager oversight. The lawyer will emphasise structures, entities, and succession planning. The accountant will focus on consolidation, reporting, and tax coordination.

Each of them is describing something real.

None of them is describing the whole picture.

Because a family office is not one thing.

It is not a legal structure you set up.

It is not a team you assemble and put on payroll.

A family office is a function. It is a discipline. And like all disciplines, it can be practised well or badly, consciously or not at all.

And the moment this function becomes necessary for a family’s wealth has very little to do with net worth alone.

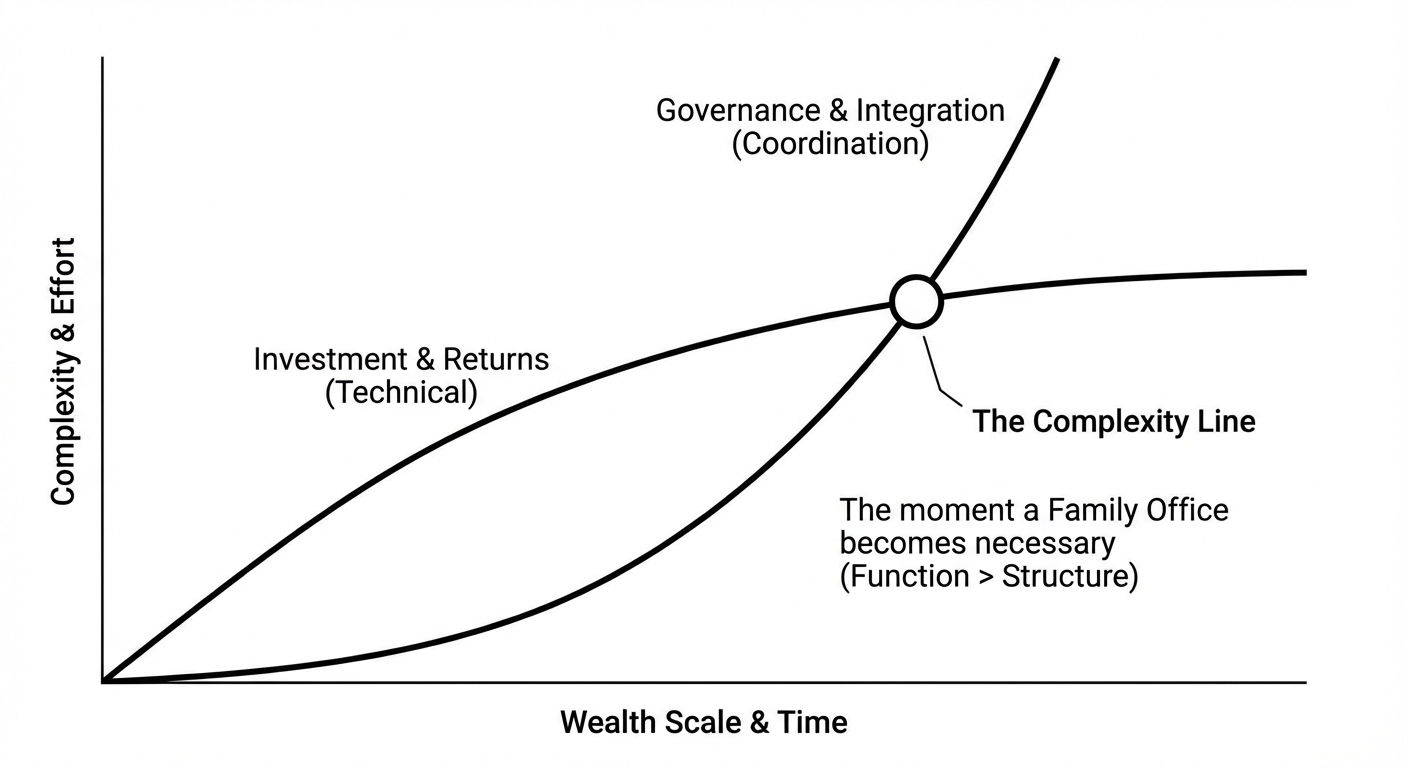

It has everything to do with crossing what I call the complexity line.

The Complexity Line

In the early stages of meaningful wealth, the work is primarily financial and technical.

The questions are clear:

- How should capital be allocated?

- How do we optimize taxes?

- How do we protect assets?

- How do we generate appropriate returns for the risk taken?

These are technical problems.

They can be handled by technical specialists.

A strong investment advisor.

A capable tax attorney.

A sharp estate planner.

A good CPA.

Each expert solves a defined problem inside a defined lane. And in this phase, that works.

Even as assets scale from $20M to $50M to $100M, the model can still hold. The complexity increases, but it increases linearly.

The portfolio grows.

The structures multiply.

The tax planning becomes more advanced.

But it is still largely technical.

And technical problems have technical solutions.

The shift nobody marks

Then something changes.

It doesn’t happen overnight.

It doesn’t trigger an alert.

It rarely shows up in a quarterly report.

But gradually, wealth stops being a financial question and starts becoming a coordination problem.

Advisors multiply.

Operating businesses, trusts, foundations, partnerships, real estate entities, investment vehicles, and cross-border structures begin to accumulate.

Different jurisdictions introduce competing rules.

Different advisors introduce different strategies.

Different family members develop different expectations.

And here is the subtle shift:

No one owns the complete picture.

Each advisor is competent.

Each file is handled.

Each return is filed.

But the integration between them becomes fragile.

That is the complexity line.

When wealth becomes structural

After this point, technical excellence is necessary but insufficient.

Because the core challenge is no longer:

“How do we optimize this?”

It becomes:

“How do we coordinate all of this?”

Who ensures the estate plan reflects the investment strategy?

Who confirms the investment strategy reflects the liquidity needs of the operating business?

Who aligns tax planning across jurisdictions?

Who governs decision-making across generations?

Who reviews whether the family’s actions match its stated objectives?

Most advisors are not incentivized to coordinate beyond their mandate.

They are not negligent.

They are specialized.

But specialization without integration creates drift.

And drift is invisible until it becomes expensive.

The costs of crossing the line

The most dangerous aspect of crossing the complexity line is that everything can still appear functional.

Taxes are filed.

Investments are managed.

Structures are compliant.

But underneath the surface:

- A tax opportunity is missed because two advisors never spoke.

- A portfolio drifts from its intended allocation because no one reviews it against a written policy.

- A liquidity event creates unnecessary tax friction because planning was fragmented.

- A next-generation family member inherits a maze of entities without context.

None of this shows up on a dashboard.

There is no notification that reads:

“Your wealth is now structurally misaligned.”

The cost compounds quietly.

And in many cases, the first visible sign of the problem is conflict, regulatory exposure, or a transition event.

By then, the complexity has hardened.

The family office misconception

When people hear “family office,” they picture an institution.

A CIO.

An investment team.

A CFO.

An in-house legal function.

For families with substantial scale, often above several hundred million in assets, a fully staffed single-family office can be appropriate.

But this image has distorted the conversation.

It has made families believe the concept is binary.

You either have one or you do not.

That framing is flawed.

Because the family office is not the structure.

It is the coordination function.

And that function can exist without a large headcount.

It can be formal or informal.

Centralized or outsourced.

Lean or institutional.

The critical question is not:

“Do we have a family office?”

It is:

“Is someone responsible for integration?”

The dollar threshold

Let me be clear, there is no universal net worth trigger.

Some families cross the complexity line at $30 million because their assets are global, illiquid, and multi-generational.

Others may not cross it until $500 million because their structure is simple and concentrated.

Complexity is not just about scale. It is about:

- Number of entities

- Jurisdictions involved

- Types of assets

- Liquidity profile

- Number of decision-makers

- Generational layers

- Philanthropic structures

- Operating businesses

Two families with identical net worth can sit on completely different sides of the complexity line.

Which means the right question is not:

“How much are we worth?”

It is:

“How complex is our reality?”

The invisible family office

In reality, every wealthy family already has a family office.

It just might be invisible.

If there is no defined coordination function, then coordination still happens. It just happens:

- By accident

- By personality

- By dominance

- By urgency

Often the founder becomes the de facto integrator.

Everything routes through them.

They hold the relationships.

They make the final calls.

They reconcile competing advice.

But that model does not scale. And it does not transfer well to the next generation.

When the integrator disappears without a system, complexity surfaces abruptly.

That is when families realize the problem was structural, not financial.

What a real family office function does

At its core, the family office function performs three roles:

1. Integration

It ensures all advisors operate within a coherent strategy.

It aligns tax, legal, investment, and estate planning decisions.

2. Governance

It defines how decisions are made.

It clarifies authority, responsibility, and succession.

It reduces ambiguity before conflict emerges.

3. Continuity

It documents frameworks.

It creates policies.

It prepares the next generation to inherit not just assets, but structure.

This is not administrative overhead.

It is structural risk management.

The emotional reality

Crossing the complexity line is not just operational. It is a psychological phenomenon.

Wealth creation feels dynamic and empowering.

Wealth coordination feels bureaucratic and heavy.

Founders often resist formalization because it feels like friction.

But structure is not constraint.

It is protection.

The absence of structure does not preserve agility. It compounds fragility.

And the longer a family waits to acknowledge that shift, the more embedded the inefficiencies become.

The real trigger

So what is the trigger for needing a family office?

It is not $50M.

It is not $500M.

It is not $1B.

It is the moment when:

- No one can articulate the full picture without preparation

- Advisors operate in parallel rather than in coordination

- Decisions create second-order effects that no one models

- The next generation lacks visibility into the architecture

It is the moment wealth becomes structural.

That is the complexity line.

And once you cross it, the question is no longer whether you need a family office.

The question is whether you are willing to build the function consciously, or continue operating an invisible one by default.

A challenge for families approaching the line

If you are a founder or a principal, pause for a moment and ask yourself these questions:

- Who owns integration?

- Where is our written investment policy?

- How often do all advisors meet together?

- Could the next generation explain our structure without you in the room?

If the answers are unclear, you may already be across the line.

Do not wait for a liquidity event, a dispute, or a generational transition to expose structural fragility.

Families who preserve wealth across generations are not the ones who hit a certain number.

They are the ones who recognized when wealth stopped being financial and started being structural.

Discussion